It’s the final week. You know you are running out of time.

Most people in the final week are still pulling things together, a missing 1099, an account statement from India, income they’re not entirely sure needs to be reported here. That’s more common than you’d think.

What’s not fine is filing without clarity. Because it gets costly the longer you wait and guess.

If you still feel like you are not ready to file, a tax expert is your fastest path forward.

Not a community forum, not a quick Google search, a conversation with someone who has dealt with your situation before.

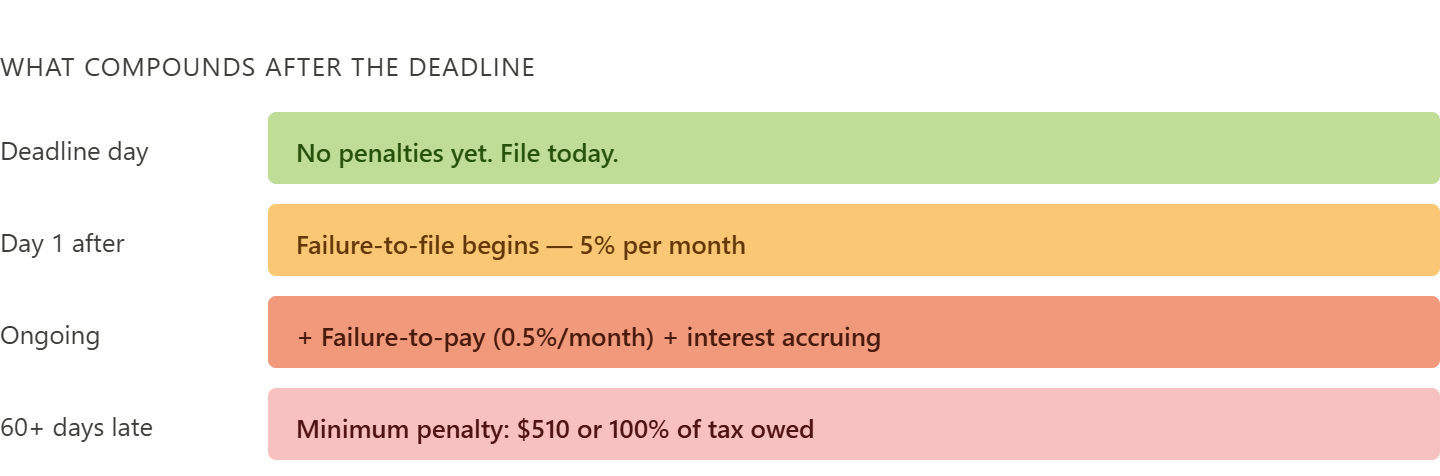

What Happens When You Miss the USA Tax Filing Deadline?

Not filing at all is more catastrophic than filing late. But acting now is better than both.

According to IRS Topic 653, the failure-to-file penalty is 5% of unpaid taxes for each month your return is late, up to a maximum of 25%.

A separate failure-to-pay penalty runs at 0.5% per month on any outstanding balance.

On top of both, interest continues to accrue, calculated at the federal short-term rate plus 3%.

In FY 2024, the IRS collected $120.2 billion in unpaid taxes and assessed $17.8 billion on late filings, with civil penalties continuing to form a significant part of overall enforcement actions. (source)

These aren’t theoretical numbers. This is what happens to tax filers who delay decisions in the final week.

“The failure-to-file penalty is 10 times the failure-to-pay penalty. File even if you can’t pay in full.” — Ed Slott, CPA

If you’re owed a refund, the exposure drops considerably. But you still need to file to get refunds.

Missing Documents? You Don’t Need the Paper. You Need the Data.

This is where most people get stuck.

One W-2 is missing.

A 1099-INT from a bank account they barely used.

Suddenly everything stops, and the assumption is – wait until it arrives.

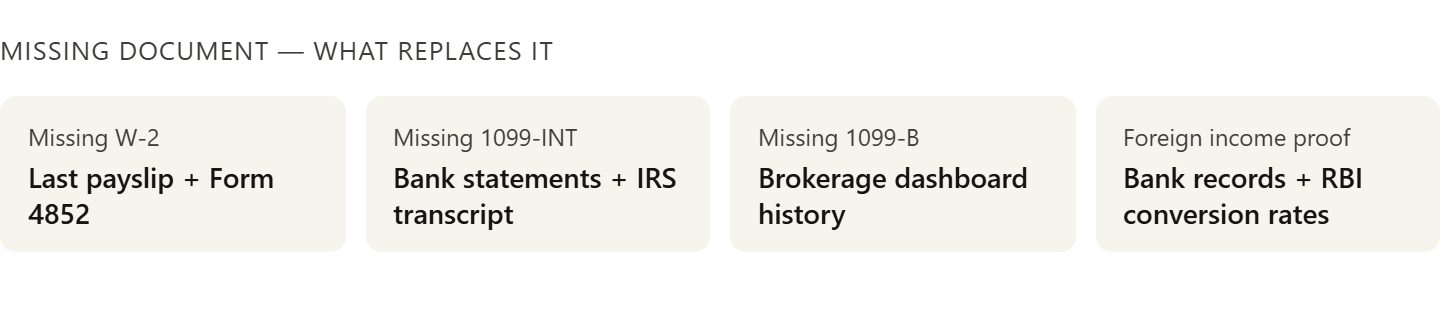

Probably your tax consultants would tell you to reconstruct required documents.

Bank statements, payslips, employer portals, and brokerage dashboards carry nearly all the data you need to file accurately.

The IRS already holds your income records on their side. If your numbers are reasonably close to what they have, you’re in a manageable position.

Form 4852 exists specifically as a substitute for a missing W-2. It’s a formal, IRS-recognized document. It’s used more often than most filers realize, including by tax consultants filing on behalf of their clients.

The IRS also provides free transcripts through their online portal. Your Wage and Income transcript shows all income reported under your Social Security number. That alone resolves issues of missing documents.

“Don’t let the perfect be the enemy of the good. An estimated, well-reasoned return beats a late, penalty-heavy one.” — Mark Luscombe, CPA, Wolters Kluwer

Most taxpayers wait for one document, and lose time for everything else that actually needs attention.

Can’t Pay What You Owe? Don’t Ignore It.

We at Crescent see this pattern often. Someone calculates what they owe, it’s more than they expected, and they decide to wait.

Thereby they turn a manageable situation into a complicated one.

Pay what you can today. The IRS offers short-term payment plans for balances that can be cleared within 180 days, no formal application required for amounts under $100,000.

For larger balances or longer timelines, installment agreements are available online through the IRS portal.

Penalties and interest still run. But you stay outside enforcement territory, which means no liens, no levies, no notices escalating toward collection.

According to the IRS, over 2.2 million taxpayers were on online installment agreements in 2024. “Taxpayers established 3.4 million new installment agreements and paid $16.1 billion toward all installment agreements in FY 2024” (source)

The option exists specifically because the IRS would rather collect over time than chase.

If you owe and aren’t sure which plan fits, you need a quick conversation with the best tax filing service, instead of figuring it out alone.

Ignoring it entirely is where situations escalate, as a payment plan controls your liability.

Missed Required Forms? This Is Where It Gets Serious.

Not filing a required disclosure form is not the same as missing a deduction. The penalties are structural, they apply regardless of how much tax you owe.

Form 5472, required for certain foreign-owned U.S. entities, carries a $25,000 penalty per missed filing. The IRS has been increasing scrutiny on this form specifically.

FBAR, FinCEN Form 114 is required if your foreign accounts crossed $10,000 on any single day of the year.

The civil penalty for a non-willful violation starts at $10,000 per violation. For willful violations, it can reach the greater of $100,000 or 50% of the account balance at the time of the violation.

FATCA reporting through Form 8938 adds another mandatory disclosure layer. If your foreign financial assets exceeded the IRS thresholds – $50,000 for single filers, $100,000 for married filing jointly, this form is not optional.

The longer these forms stay unfiled, the more exposure compounds. First-time penalty abatement and reasonable cause relief exist, but both require you to act before the IRS contacts you.

“The IRS is increasing its focus on offshore accounts. Non-filers are at greater risk than ever of detection.” — Nina Olson, former National Taxpayer Advocate

For Indian NRIs and NRI Professionals in the U.S., What Most People Miss?

This is where the complexity is the highest, and most last-minute tax filing mistakes happen.

Indian NRIs and H1B professionals working in the U.S. often carry financial ties to India that significantly affect their US return, and are often the last thing reviewed before filing.

- Rental income from a property in Bangalore.

- Dividends from Indian stocks.

- Proceeds from a mutual fund redemption.

- Capital gains from a property sale before moving.

Each of these is reportable on your U.S. return. The U.S. taxes on worldwide income, residency status doesn’t change that.

If your NRE or NRO account, Indian savings account, or PPF balance crossed $10,000 on any single day, FBAR compliance becomes mandatory, regardless of whether you transferred money in or out that year.

PFIC rules apply to Indian mutual funds held in your name. The IRS classifies most Indian mutual funds as Passive Foreign Investment Companies.

The tax treatment under PFIC rules is significantly more punitive than for domestic funds, and it’s not something that shows up intuitively when you’re filing on your own.

“Cross-border filers face a different tier of complexity. The forms themselves carry penalty exposure that the tax owed doesn’t.” — Gary Carter, CPA, International Tax Specialist

Rushing through this section in the final hours leads to chaos for NRIs in the USA.

Filed Incorrectly? The Fix Takes Longer Than the Mistake

Corrections are normal. The IRS processes thousands of amended returns every year.

But here’s what most people don’t account for: Form 1040-X, the amendment form, takes the IRS up to 20 weeks to process when filed by mail. Even electronically, it takes weeks. During that time, your refund is held.

If something in your return feels off right now, a form you’re unsure about, foreign income categorized incorrectly, review it now or seek last-minute tax consultant support before you submit.

Once it’s filed, you’re in the amendment queue, and corrections are on the IRS’s timeline.

Filing right once takes more effort upfront. Fixing it later takes significantly more time, follow-up, and in some cases, professional involvement to unwind what went wrong.

Final Week Mistakes That Cost More Later

Why do you wait for one document while ignoring everything else that’s ready?

- Skipping foreign income because it “probably” doesn’t need to go on the U.S. return.

- Guessing on numbers instead of reconstructing from available data.

- Ignoring required forms because they weren’t on last year’s return.

- Rushing the cross-border section because it feels complicated.

Every year, millions of taxpayers request extensions—often because their filings involve complexity that can’t be resolved in the final week.

But an extension only delays filing, not payment. If you owe, interest and penalties continue to accumulate from the original deadline.

If you’re rushing right now, you’re more likely to miss exactly the things that matter most. That’s not urgency talking; it’s a pattern that cross-border tax experts see every year in amended returns filed in May and June.

Before You Submit, Check This!

Five things, five minutes. Go through this checklist before you hit ‘submit’.

- Correct form for your filing status.

- All income included – domestic and foreign.

- Foreign accounts reviewed against FBAR and FATCA thresholds.

- Missing or required forms addressed.

- Payment or extension decision made if a balance is owed.

This check has prevented more costly errors than any single piece of tax advice.

FAQs

1. What happens if I don’t file by April 15th?

Missing April 15 triggers a failure-to-file penalty of 5% per month (up to 25%), plus a 0.5% monthly failure-to-pay penalty on unpaid taxes. Interest accrues on top until the balance is cleared.

2. Can I file taxes late in the USA?

Filing late is allowed at any time. Penalties and interest apply if taxes are owed, but filing sooner reduces additional charges. Refund cases generally avoid penalties, though filing is still required to claim the refund.

3. What happens if you forget to file your taxes in the USA?

Forgetting to file leads to accumulating penalties and interest if taxes are owed. The IRS may also file a substitute return on your behalf, often without deductions or credits, resulting in a higher tax liability.

4. Can I e-file after the deadline?

E-filing remains available for current-year returns even after the deadline, though availability depends on IRS systems and providers. Late filing penalties still apply if taxes are owed, regardless of how the return is submitted.

5. What is the IRS penalty for late filing?

The failure-to-file penalty is 5% of unpaid taxes per month, capped at 25%. A separate failure-to-pay penalty of 0.5% per month applies, along with interest calculated at the federal short-term rate plus 3%.

Conclusion

If you have made it till the end, you should understand, it’s all about making the right decisions with what you have.

This is where many filers, especially Indian NRIs handling cross-border income run into trouble. Because the final days’ stress compress decisions that need clarity.

Crescent Tax works closely with filers experiencing these situations every tax year, where information is incomplete, filings involve FBAR or FATCA exposure, or key details still feel uncertain.

With an IRS-approved e-file setup, Crescent Tax has helped over 27,000 Indians in the U.S. With a team of 85+ tax preparers, the focus stays on getting filings right before submission, not fixing them later.

If something in your return still feels unclear, opt for the guidance from professional tax consultants to save yourself from hefty IRS penalties later.

Disclaimer: Tax laws are complex and subject to change. Always consult a professional cross-border tax advisor (CPA or Enrolled Agent) specializing in US-India taxation for specific cases.