Are you still holding bank accounts in India while living in the U.S.?

If yes, don’t let tax reporting season become a compliance headache. You’re reading this at the right time.

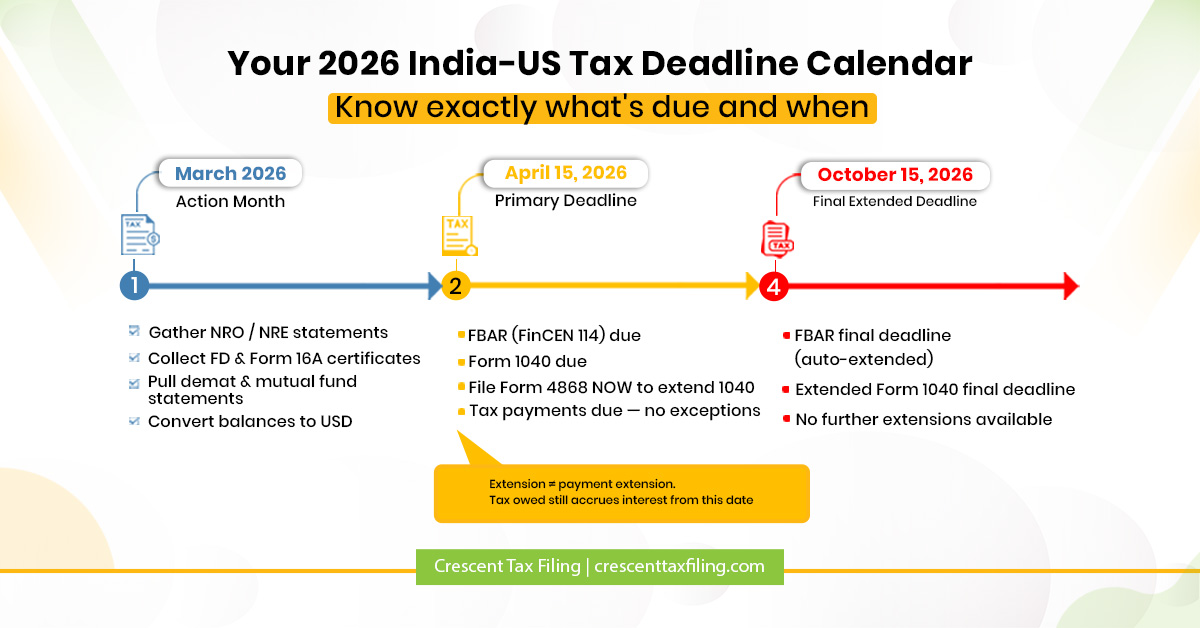

March is when smart filers get clarity in foreign account reporting. You need to file FBAR (FinCEN Form 114) and Form 8938 (FATCA) along with other obligations. Delay in reporting these brings in substantial penalties.

This blog will share what applies to you and what to prepare now. So that you stay compliant and know when it’s time to consult the best tax expert.

If I Have Bank Accounts Back in India, Am I Required to Report Them to the IRS?

Every Indian in the USA holding foreign financial accounts is required to report them to the IRS. This obligation applies whether those accounts are active, dormant, or held jointly with family back home.

H-1B, L-1, F-1 visa holders, green card holders, and US citizens all fall under this rule. The US taxes its residents’worldwide income; that NRO, NRE accounts, that FD, that joint account your parents manage back home.

All of it needs to be reported to the IRS and to FinCEN. With April 15, 2026 just weeks away, now is the right time to find out where you stand.

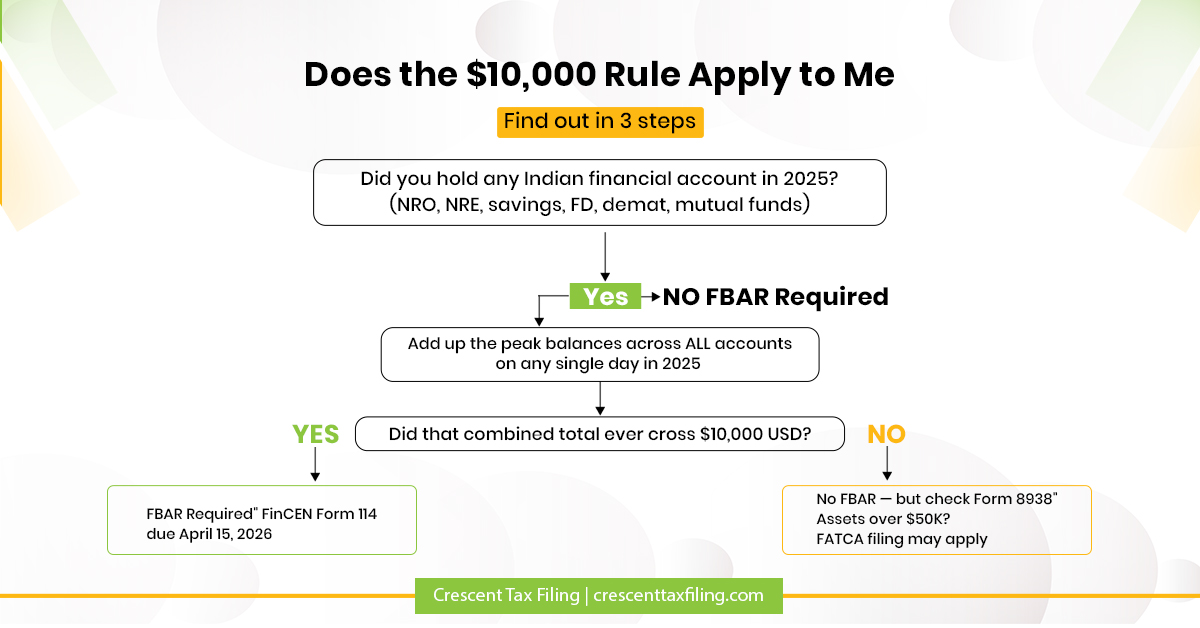

How Exactly Does the $10,000 Threshold Work? Is It Per Account or Combined?

The $10,000 threshold is combined, not per account. It is the aggregate maximum balance across all your foreign financial accounts, measured at any single point during 2025, even for one day. This is where most Indians working in the USA get caught off guard.

| For Example,

Say you had ₹4,00,000 in your NRO account and ₹4,50,000 in an NRE savings account in June 2025. At the prevailing exchange rate, that combined balance likely crossed $10,000 USD — making FBAR filing mandatory for the entire 2025 calendar year, even if both accounts are now near zero. |

Which of My Indian Accounts Actually Need to Be Included in That Balance?

More account types qualify than most people expect, and the list goes well beyond just your primary savings account.

- NRO and NRE savings accounts

- Fixed Deposits (FDs) — each FD is counted as a separate account

- Demat and brokerage accounts (Zerodha, Groww, HDFC Securities, ICICI Direct, etc.)

- Mutual fund folios held directly

- Joint accounts — even those held jointly with parents or a spouse in India

- Accounts where you only have signing authority, such as a family business account

PPF and EPF accounts have different treatment and are generally not included in the FBAR calculation, though the income from them may still be reportable.

Many Indians in USA are unsure which accounts qualify. A tax expert familiar with India-US cross-border taxation can clearly explain it to you.

Does Filing the FBAR Also Cover the Income My Indian Accounts Earned?

The FBAR only discloses that the account exists. It does not report the income it earned. These are two separate obligations, and both are required.

This distinction surprises many Indian workers in the U.S. who assume filing the FBAR completes their compliance picture.

Your Form 1040 with Schedule B is where interest income from Indian accounts is reported. The IRS cross-references Schedule B against your FBAR, inconsistencies raise flags.

If your Indian FD earned interest in 2025, even if that interest was never transferred to the US, it must be declared on Schedule B of your US tax return, converted to USD using the IRS Treasury exchange rate.

What Is the Full Set of Forms Indians in USA Need to File for Indian Accounts?

There is no single form. There are three layers of compliance, and which ones apply depends on your accounts, income, and assets. Quality tax filing services for Indians in USA structure the return across all three layers.

| Layer 1 — Mandatory | Layer 2 — Tax Return | Layer 3 — Situational |

| FBAR (FinCEN 114)

Form 8938 (FATCA) Disclosure filings — threshold based |

Form 1040 / 1040-NR

Schedule B Schedule E (if rental income) Form 4868 (if extending 1040) |

Form 1116 (TDS credit)

Form 8621 (Mutual Funds/PFIC) Form 3520 (Gifts/Inheritances) |

Layer 1 is mandatory for anyone above the threshold. Layer 2 ties into your tax return. Layer 3 is situational.

My Indian Bank Already Deducted TDS, Will I Be Taxed Again on the Same Income in the US?

The TDS your Indian bank already deducted can be applied as a credit against your US tax liability on the same income to avoid double taxation. Form 1116 (the Foreign Tax Credit) is the mechanism that makes this work.

You still need to declare the Indian income on Schedule B, the credit offsets the tax owed, it does not eliminate the reporting requirement. While Form 1116 allows you to claim credit for taxes already paid in India, the actual benefit depends on how accurately it is calculated and reported.

Tax experts take care if you underclaim credits, lose carryforwards, or create mismatches that could trigger IRS scrutiny.

If I Hold Indian Mutual Funds, ULIPs, or PPF., Will It Trigger Additional IRS Filing Requirements?

Indian mutual funds and ETFs are classified as Passive Foreign Investment Companies (PFICs) by the IRS. This means every folio you hold requires a separate Form 8621 filing. ULIPs with underlying funds are treated the same way.

PPF accounts are generally exempt from FBAR but may still generate reportable income under FATCA reporting rules depending on your total asset threshold.

If you hold any of these instruments, working with tax consultants who understand both Indian investment structures and US international tax rules prevents you from paying taxes twice. Get in touch today!

Do I Need to Report to the IRS The Money Received From Family in India?

Gifts or inheritances from Indian family members totalling more than $100,000 during 2025 must be reported on Form 3520. This is one of the most frequently missed filings among Indians in USA, entirely separate from FBAR and Form 8938.

There is generally no tax owed on the gift itself in Form 3520, but the failure-to-file penalty is severe; 5% of the gift amount per month, up to 25%.

What Happens If I Have Missed Filing in Prior Years. Is There a Way to Fix It?

Prior year non-filing can be corrected through the IRS Streamlined Filing Compliance Procedure. This program is designed for Indian descent residing in the USA and other foreign nationals who missed FBAR or income reporting obligations without willful intent. Acting before the IRS contacts you is what makes this option available.

In case of penalties, non-willful FBAR violations carry up to $16,536 per report for 2026, and following the 2023 Supreme Court ruling in Bittner v. In the United States, this is per report, not per account.

Willful violations reach $100,000 or 50% of the account balance, whichever is greater. The window closes the moment the IRS contacts you first.

With April 15 Just Weeks Away, What Should I Be Doing Right Now?

Gather every Indian account document for the January–December 2025 calendar year, not the Indian financial year. As the IRS deadline countdown begins, this is the right time to review everything carefully before filing.

- NRO and NRE account statements — full calendar year January–December 2025

- Collect Fixed Deposit certificates and interest/TDS certificates (Form 16A from your Indian bank)

- Pull demat and mutual fund statements showing balances and income

- Convert all peak balances and income figures to USD using the IRS Treasury year-end exchange rate

- Check whether you received any gifts or transfers from family in India exceeding $100,000

- Confirm whether you hold Indian mutual funds — each folio may need a Form 8621

- File or schedule your FBAR and Form 1040 with a qualified tax professional before April 15

FAQs

-

What happens if I have more than $10,000 in a foreign bank account?

Once the combined balance across all your foreign accounts crosses $10,000 at any point during the year, FBAR filing becomes mandatory. The threshold is aggregate, not per account. It applies even if the balance drops back down before year-end.

-

What is the IRS update for 2026?

For the 2025 tax year, the FBAR deadline remains April 15, 2026, with an automatic extension to October 15. Non-willful penalty amounts are inflation-adjusted to $16,536 per report, following the Bittner ruling that confirmed penalties apply per report, not per account.

-

What is the penalty for not filing a foreign bank account?

Non-willful violations carry penalties up to $16,536 per report for 2026. Willful violations are significantly higher; the greater of $100,000 or 50% of the account balance. Coming forward proactively through the IRS Streamlined Filing Procedure can substantially reduce or eliminate these penalties.

-

Do I have to report my NRO account to the IRS?

An NRO account must be included when calculating your combined foreign account balance. If that aggregate total exceeded $10,000 at any point in the current calendar year (in this case, 2025), FBAR filing is required. Interest earned on the NRO account must also be reported on Schedule B of your US tax return.

Conclusion

Crescent Tax Filing has more than 95% satisfaction rate in helping 27000+ Indians in USA since the past 8 years.

As choosing the right professional tax services means nothing gets missed and no deadline goes unmanaged.

Our experienced tax preparers understand both the Indian financial landscape and US tax laws. So whether you are filing for the first time or coming into compliance for prior years, nothing falls through the cracks.

Contact our professional tax consultants at Crescent Tax Filing, as April 15 is closer than it feels.

Disclaimer: This blog is for general informational purposes only and does not constitute tax, legal, or financial advice. Please consult a qualified tax professional for guidance specific to your situation.