The deadline is easy to see.

The hidden risks are not.

For most individual filers, the IRS deadline for tax year 2025 is April 15, 2026. The IRS also says that this is the deadline to file and pay for most taxpayers.

What many Indians in USA miss is not the date. It is the work that should happen before the date.

I have seen the same pattern for years. People focus on the return itself. Then, late in the season, they realize the real problem is somewhere else:

- an Indian bank account they forgot to count

- a fixed deposit they thought did not matter

- a joint account they assumed was not theirs

- a residency issue they never checked

- a missed FBAR filing

- skipped FATCA reporting

That is where risk starts.

If you need a broad filing starting point before you get into the foreign-account side, Individual Tax Filing is the right place to begin.

Why do Indians in USA ignore hidden FBAR filing risks?

Most people do not think in totals.

They think in separate accounts.

That is the first mistake.

The IRS says FBAR filing may be required if the combined value of foreign financial accounts goes above $10,000 at any point during the year. The IRS also says the FBAR is due on April 15 and gets an automatic extension to October 15 if missed.

That means the review must include all foreign accounts together.

For many Indians in USA, that may include:

- NRE accounts

- NRO accounts

- savings accounts

- fixed deposits

- certain brokerage accounts

- joint family accounts

A person may say, “I only have one small account.”

Then the review shows:

- one NRE account

- one NRO account

- one old fixed deposit

- one joint account

None looks large alone. Together, they cross the line.

That is why FBAR filing becomes a hidden risk. It hides inside small balances.

If you want that filing cycle put in plain terms, FBAR Filing for Indians in USA is a useful checkpoint. If old years may have been missed, Late FBAR Filing should be part of the review before anything is filed.

Why does FATCA reporting stay hidden until the return looks done?

Because many filers think income reporting and asset reporting are the same thing.

They are not.

The IRS says Form 8938 is used to report specified foreign financial assets when the value goes above the reporting threshold that applies to the taxpayer. The IRS also says Form 8938 and FBAR are separate requirements, and one does not replace the other.

That creates a common problem.

A return may look complete because:

- salary is reported

- bank interest is reported

- investment income is reported

But the return can still be incomplete if the foreign asset disclosure side was never checked.

That is why FATCA reporting is a hidden risk. It often does not feel urgent until the return is already in progress.

For a clean first pass on the larger filing process, US Tax Filing basics should be kept in view.

Why do tax consultants treat residency as a hidden risk?

Because people often guess.

That is the problem.

Many Indians in USA assume immigration status and tax residency mean the same thing. They do not.

Residency can affect:

- whether worldwide income is reportable

- whether FATCA reporting thresholds matter

- whether a treaty position makes sense

- What kind of return should be filed?

I have seen returns where the filer spent time worrying about one Indian account, while the bigger issue was that the residency position itself had not been checked.

That is not rare.

That is why Resident vs Non-Resident belongs near the start of the review, not near the end.

And when the facts are not simple, Tax Consultations is the better move than filing based on guesswork.

Why do professional tax services catch risks that filers miss?

Because hidden risks are usually process problems before they become tax problems.

They often begin with small things:

- One missing statement

- one old account

- One balance that was only high for a short time

- One joint account, nobody counted

- One asset that was treated like “not important.”

Then those small things become filing problems because they were never reviewed in the right order.

Good professional tax services follow a clean sequence:

- gather all records

- confirm residency

- List all foreign accounts and assets

- test FBAR filing

- test FATCA reporting

- Prepare the return

- review filing and payment timing

That order matters.

When that order is broken, the return may move faster, but the risk gets bigger.

For the main filing path, US Tax Filing is the clearest service to approach. If audit exposure or notices are already part of the case, Tax Audit Services becomes more relevant.

Why is the best tax filing service not always the fastest one?

Because fast filing can hide a weak review.

The best tax filing service is not the one that sends a return first. It is the one that checks what could later create problems.

That includes:

- foreign balances

- ownership

- reporting thresholds

- residency

- payment timing

I have seen quick filings that later needed:

- amended returns

- separate foreign reporting fixes

- cleanup work that took longer than the original filing

That is why the hidden risks matter more than the filing speed.

If the season still feels early, IRS Deadline 2026 is the right place to reset the timeline before pressure builds.

Why is payment a hidden IRS deadline risk for Indians in USA?

Because people often focus only on filing.

The IRS says April 15, 2026 is the deadline to file and pay for most taxpayers. The IRS also says that if you request an extension, you get more time to file, but not more time to pay tax due.

That means a taxpayer can still create a problem even if the return is not technically late.

A common example:

- the person files an extension

- assumes the main pressure is gone

- does not estimate and pay what is due

- later gets hit with interest and penalties

That is a deadline risk, but it often feels hidden because the person thinks the extension solved everything.

It did not.

Extensions help with filing time. They do not erase payment duties.

If someone is already near or past the line, good to know what happens when you Missed IRS Deadline.

Why do Indians in USA ignore old accounts and inactive accounts?

Because it feels harmless.

That is the trap.

An inactive account is not the same as a closed account.

A balance that sits untouched can still matter.

Here are the most common hidden-account issues I see:

Old NRO account

Used years ago, barely checked now, still holds money.

Fixed deposit

Not part of daily banking, so people forget to count it.

Joint family account

The taxpayer says the funds are “not really mine,” but the name is still on the account.

Broker account with no trades

No recent activity, but assets are still there.

This is why early account review matters more than deadline pressure. Hidden risks almost always sit in places people stopped looking at.

Why does FBAR filing become a bigger problem when people wait too long?

Because FBAR filing depends on records, not memory.

The IRS rule is simple. The calculation is not always simple.

To file properly, a person may need:

- full-year statements

- peak balance review

- account ownership review

- a list of all qualifying accounts

If the review starts too late, people begin to estimate:

- “I think the balance never crossed the line.”

- “That account probably stayed low.”

- “I do not think that joint account counts.”

That is weak filing logic.

If the account data is still incomplete in the last week, the danger is not just a late filing. The danger is a careless one.

That is why early review is not optional in foreign-account cases.

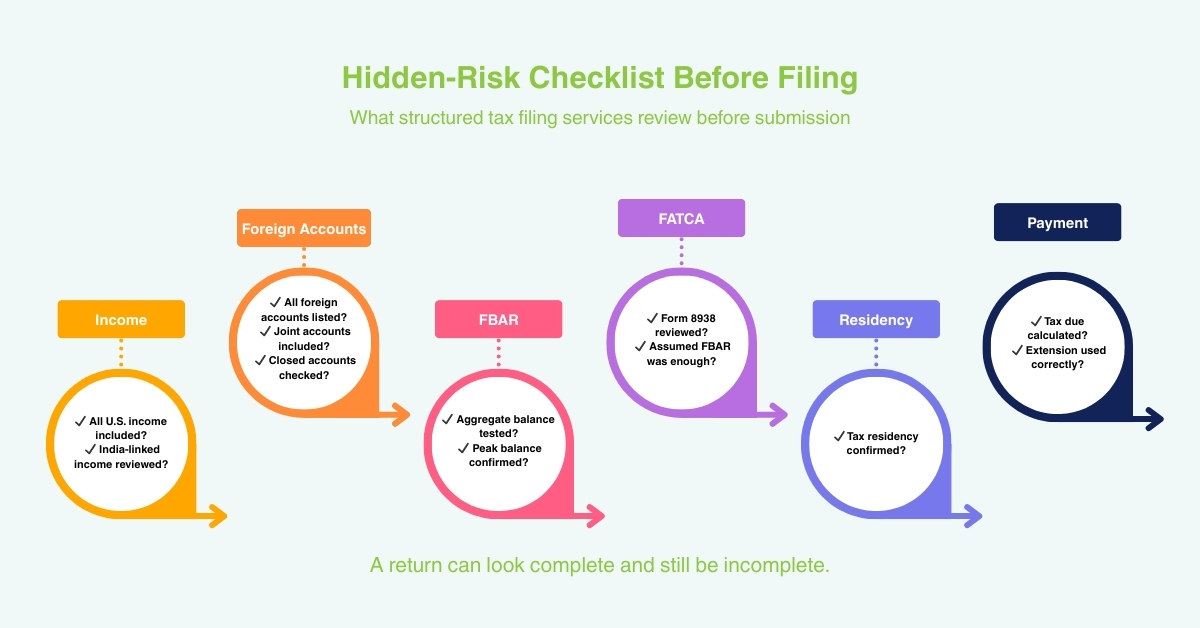

Why do tax filing services need a hidden-risk checklist before submission?

Because the return itself can hide what is missing.

Before any return is filed, the final review should answer these questions:

Income

- Did you include all U.S. income?

- Did you include India-linked taxable income where required?

Accounts

- Did you list all foreign accounts?

- Did you include joint accounts?

- Did you check whether closed accounts existed during the year?

FBAR filing

- Did the aggregate balance cross $10,000 at any point?

- Did you use real balances instead of year-end assumptions?

FATCA reporting

- Did you check whether any foreign assets require Form 8938 review?

- Did you assume FBAR was enough without checking?

Residency

- Is your filing position based on confirmed tax residency?

Payment

- If tax is due, are you prepared to pay by the deadline?

- If you need an extension, are you using it correctly?

This kind of checklist is exactly why structured tax filing services are valuable. It keeps hidden risks from staying hidden.

Why do Indians in USA ignore treaty issues until it’s too late?

Because treaty review feels technical, people push it down the list.

But treaty questions can matter when someone has:

- India-source income

- foreign tax already paid

- dual-country reporting concerns

- uncertainty about what gets taxed where

The U.S.-India treaty does not replace FBAR filing or FATCA reporting. It does not remove disclosure rules. But it can still matter when a return is built.

If treaty concerns are part of the case, US India Tax should be part of the review before final decisions are made.

Why does a seasoned tax expert worry more about hidden risks than obvious ones?

Because obvious risks are usually easier to fix.

If someone knows they are late, they can act on that.

If someone does not know they missed:

- FBAR filing

- FATCA reporting

- a residency issue

- a payment issue

- a reporting threshold

The problem can sit quietly and grow.

That is why I always treat hidden risks as more important than the visible deadline pressure.

The visible deadline is one day.

The hidden mistakes can follow the taxpayer for much longer.

FAQs

What is the IRS deadline for 2026 returns?

For most individual calendar-year filers, the deadline for tax year 2025 returns is April 15, 2026. The IRS also says this is the deadline to pay tax due in most cases.

What hidden risk do Indians in USA ignore most often?

The most common hidden risk is incomplete foreign-account review. That usually leads to missed FBAR filing checks or missed FATCA reporting review.

Is FBAR filing the same as FATCA reporting?

No. The IRS states that they are separate requirements. One does not replace the other.

Do small Indian accounts still matter?

Yes. The IRS says the FBAR filing rule is based on the combined value of foreign accounts, not one account alone.

Can an extension remove the risk if I am not ready?

No. The IRS says an extension gives more time to file, not more time to pay tax due.

Why do tax consultants review residency first?

Because residency affects what income and foreign assets must be reviewed. If the residency position is wrong, the rest of the filing may also be wrong.

Final word

The IRS deadline is not hidden.

The hidden risks are:

- foreign accounts that were not fully counted

- FBAR filing that was never tested

- FATCA reporting that was assumed away

- residency that was guessed

- payment that was postponed without a plan

For many Indians in USA, these are the real risks that deserve attention before the deadline.

That is why the safest filing season is not built on speed.

It is built on review.

If you are an Indian in USA and want clarity before filing, speaking with a qualified Tax Accountant can help you review hidden risks before they become problems.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional tax advice. Tax rules and reporting rules can change. You should review your specific facts with a qualified tax expert, tax consultants, or a provider of professional tax services before making filing decisions.