The date is visible. The weak spots are not.

For most individual filers, the federal due date for tax year 2025 is April 15, 2026. The IRS also says that date is generally the deadline to both file and pay.

That sounds simple. In practice, this is the stage where many Indians in USA discover that the return itself is only one part of the work. The bigger issues usually sit behind the return:

- foreign accounts that were never added together

- asset disclosure that was never checked

- Residency assumptions carried over from last year’s

- payment timing, which was treated as an afterthought

Those are the things that create trouble close to the deadline.

If the filing process still feels scattered, Individual Tax Filing is a clean first step because it brings the return back into order before the deadline starts forcing rushed decisions.

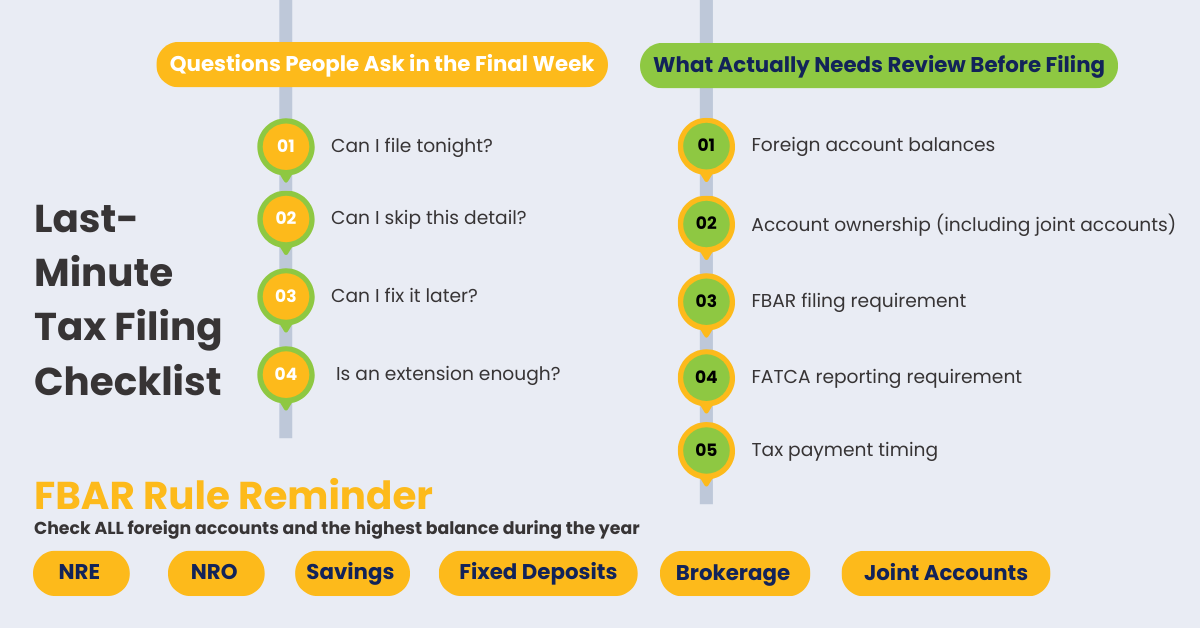

Tax filing services: What should be reviewed first when the IRS Deadline 2026 gets close?

The first review should not be the tax software.

It should be the facts.

That means confirming:

- What income belongs on the return

- What accounts exist outside the U.S?

- whether any foreign assets trigger extra disclosure,

- whether the filing position still matches the current year

This is where many tax filing services cases go wrong. People try to “start filing” before they have finished “checking.”

That order creates weak returns.

A steadier way to approach the season is to be aware of the IRS Deadline 2026.

FBAR filing: Why do so many Indians in USA discover this too late?

Because people usually think account by account.

The rule does not.

The IRS says FBAR filing may be required if the combined value of foreign financial accounts exceeds $10,000 at any point during the year. The IRS also confirms that the FBAR due date is April 15, with an automatic extension to October 15.

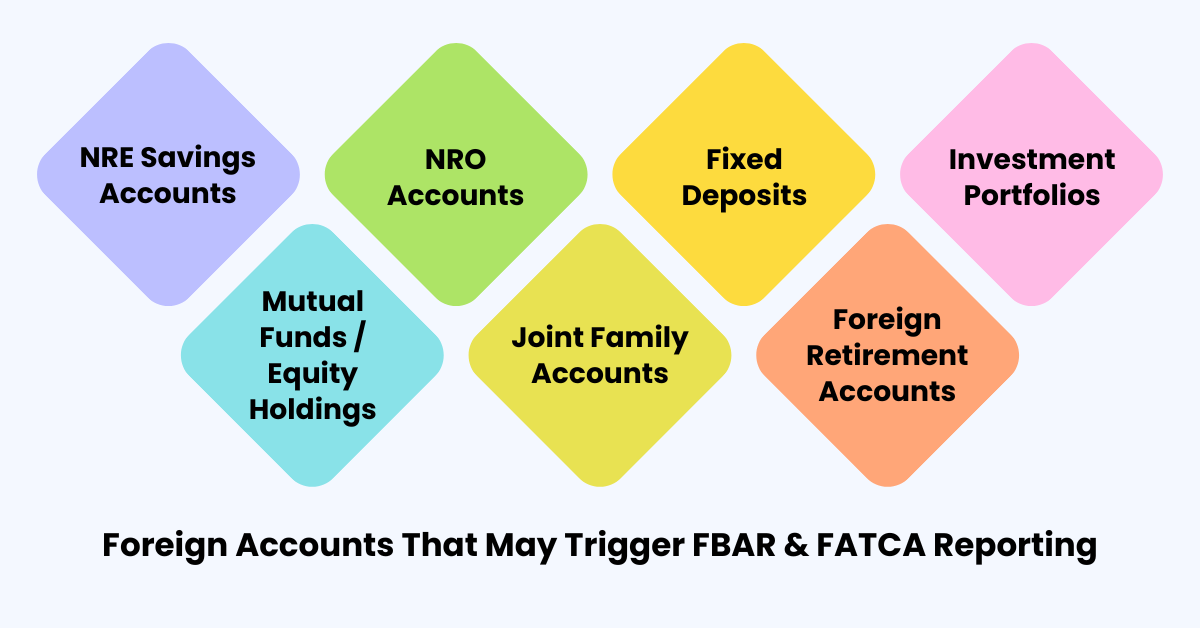

That means the review has to include the total picture, not one balance in isolation.

Common examples include:

- an NRE account

- an NRO account

- a fixed deposit

- a joint family account

- a dormant brokerage account

Individually, these may look ordinary. Together, they can cross the threshold and trigger FBAR filing.

This is why the risk stays hidden until late. The accounts do not look large enough one by one, so they are not reviewed as a group.

The annual filing pattern becomes much easier to understand when it is put in one place. Know the FBAR Filing for Indians in USA because it connects the tax return and the foreign account review in the same cycle.

If older years are part of the concern, knowing Late FBAR Filing is a smart move.

FATCA reporting: What gets missed when the return looks almost done?

A return can be complete on income and still incomplete on disclosure.

That is where FATCA reporting creates problems.

The IRS says Form 8938 is used to report specified foreign financial assets if the value goes above the reporting threshold that applies to the filer. The IRS also says Form 8938 and FBAR are separate requirements, and one does not replace the other.

That means a person can:

- report foreign interest

- report foreign dividends

- report income correctly

and still miss FATCA reporting.

This happens most often when someone thinks foreign income reporting and foreign asset reporting are the same thing. They are not.

A practical example:

- a filer reports interest from an Indian account

- assumes the foreign side is done

- never checks whether total foreign assets require Form 8938 review

That is the kind of error that does not feel obvious until a full review is done.

For the broader filing base around foreign accounts and foreign income, knowing the basics of US Tax Filing belongs in the process before the return is treated as final.

Tax expert: Why should residency be checked before the return is finalized?

Because residency is not just a background detail.

It changes what the return is built on.

A lot of people assume immigration status and tax status mean the same thing. They do not. Residency can affect:

- whether worldwide income is reportable

- whether FATCA reporting thresholds matter

- whether a treaty review makes sense

- Which form is even appropriate

That is why a tax expert should not leave this question until the return is almost finished.

I have seen cases where the filer spent time worrying about one small foreign balance when the bigger issue was the filing position itself. Once the residency conclusion changed, the rest of the return had to be reviewed again.

That is exactly why Resident vs Non-Resident should be part of the early checklist, not a late fix.

Professional tax services: What do they catch that a rushed filer often misses?

Usually, they catch the weak links in the sequence.

The most common last-stage errors are not complicated legal problems first. They are process problems first:

- starting the return before all records are gathered

- entering U.S. income while the foreign-account list is still incomplete

- Treating one account as unimportant because it is old or inactive

- assuming one report covers both FBAR filing and FATCA reporting

- waiting until the return is nearly done to ask whether residency changed

This is why good professional tax services do not just “prepare.” They control the order.

A strong review usually goes:

- gather all records

- Confirm filing position

- List foreign accounts and assets

- test FBAR filing

- test FATCA reporting

- Prepare the return

- Review payment timing

That order keeps one forgotten detail from becoming a larger correction later.

Tax consultants: Why do they focus on account ownership, not just account balances?

Because balance alone does not answer the reporting question.

Ownership matters.

This is one of the most common blind spots for tax consultants to correct. People often say:

- “It is only a joint account.”

- “It is mainly family money.”

- “My name is there, but I do not really use it.”

That kind of thinking creates filing errors.

A joint account may still need review. A family-linked account may still matter. A rarely used account may still count if it exists during the year and affects thresholds.

This is one reason hidden risks stay hidden: the filer mentally removes accounts from the review before the rules do.

That is also why it is a mistake to wait until the final days to sort ownership questions. Those questions are not hard, but they do need time.

Best tax filing service: Why is speed the wrong goal near the deadline?

Because speed can create a false sense of safety.

The best tax filing service is not the one that files first. It is the one that checks the filing before it is sent.

That means slowing down where it matters:

- foreign balances

- account ownership

- residency

- FBAR filing

- FATCA reporting

- payment timing

Fast filing can still lead to:

- amended returns

- separate foreign reporting corrections

- Extra explanation later because the first review was weak

The return may be filed. The risk may still be open.

That is why the last part of the countdown should not be about “how fast can this be sent?” It should be about “what still has not been tested?”

Tax filing services: Why is payment timing one of the most ignored deadline risks?

Because many people focus only on the act of filing.

The IRS says April 15 is generally the deadline to file and pay for most taxpayers. The IRS also says that if more time is needed to file, taxpayers should request an extension, but that does not extend the time to pay tax due.

That creates a very common mistake:

- The filer requests an extension

- feels that the deadline pressure is handled

- delays payment

- Later faces interest or penalties

This is not a rare problem. It is one of the quiet ways the deadline still causes damage even when the return itself is not technically late.

That is why every last-stage checklist should split this into two separate questions:

- Is the return ready to file?

- Is the payment ready to make?

Treating those as one question is a major error.

Why do small foreign accounts become big filing problems?

Because “small” is not the real test.

The real test is whether the account changes a filing obligation.

This is where people get caught:

- an old NRO account with a modest balance

- a fixed deposit that has not moved in months

- a joint family account used rarely

- a foreign brokerage account with no recent trades

Each one feels minor.

Then one of them:

- pushes the total above the FBAR filing threshold

- becomes part of a broader FATCA reporting picture

- changes the completeness of the return

That is why these are not harmless details. They are threshold details.

And threshold details are exactly what people ignore when the countdown gets short.

Why does a seasoned tax expert worry more about hidden risks than obvious ones?

Because obvious problems are easier to act on.

A person who knows they are filing late can respond to that.

A person who does not know they missed:

- FBAR filing

- FATCA reporting

- a payment issue

- a residency issue

- an ownership issue

can file with confidence and still have a weak return.

That is the real danger.

The visible deadline is one date.

The hidden filing mistake can stay alive much longer.

That is why a seasoned tax expert spends more time checking what the filer has not noticed yet than what the filer already expects.

FAQs

What is the IRS deadline for tax year 2025 returns?

For most calendar-year individual filers, the deadline is April 15, 2026. The IRS also says this is generally the date to file and pay.

Is FBAR filing the same as FATCA reporting?

No. The IRS states they are separate requirements, and one does not replace the other.

What should be reviewed first during the IRS deadline countdown?

Start with the facts: full income, full foreign-account list, residency, and whether FBAR filing or FATCA reporting applies.

Why do tax consultants focus on joint accounts?

Because ownership can affect whether an account needs review, even if the money does not feel “personally used.”

Can an extension solve a deadline problem?

It can help with filing time, but the IRS says it does not extend the time to pay tax due.

What makes the best tax filing service close to the deadline?

A process that checks the facts before submission. Near the deadline, speed without review creates risk.

Final word

The countdown itself is not the problem.

The problem is what goes unchecked during the countdown.

For many Indians in USA, the real issues are:

- foreign balances that were never added together

- FBAR filing that was never tested

- FATCA reporting that was assumed away

- residency that was guessed

- payment that was delayed without a plan

That is why the strongest filing is not built on pressure.

It is built on review.

If you want to review your FBAR or FATCA situation this March, a quick conversation with a tax expert can give you the clarity and confidence to move ahead.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional tax advice. Tax laws and reporting rules can change. You should review your specific facts with a qualified tax expert, tax consultants, or a provider of professional tax services before making filing decisions.