The closer April 15 gets, the more people focus on the tax return itself.

That is understandable, but it is not always where the real issue sits.

If you have foreign accounts, foreign deposits, or financial ties outside the United States, the better question is not, “Is my return almost done?” The better question is, “Is my FBAR filing actually ready?”

For tax year 2025, most calendar-year individual filers must file by April 15, 2026. The IRS states that clearly on its filing page.

For many households with cross-border finances, the filing deadline is not the only thing that matters. What matters just as much is whether the foreign-account side has been handled correctly before that date arrives.

That is where the problems begin:

- an account was left off the list

- a balance was checked at year-end instead of peak value

- a joint account was treated like it did not matter

- FATCA reporting was assumed to be the same as FBAR filing

- payment timing was never separated from filing timing

If you need a clear starting point before the deadline narrows your options, tax filing services is the right place to begin.

What does “FBAR ready” actually mean before April 15?

A lot of people think being “ready” means they know they have foreign accounts.

That is not enough.

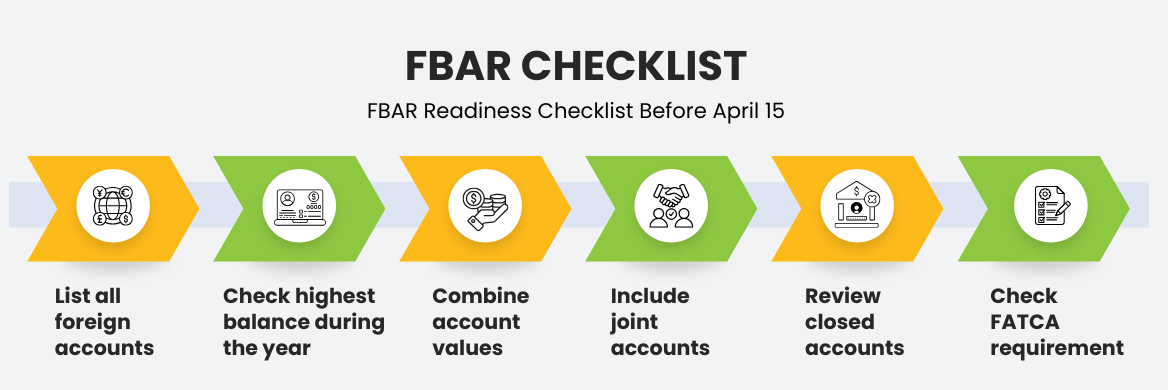

Being ready for FBAR filing means you can answer these questions clearly:

- Which foreign financial accounts existed during the year?

- What was the highest balance in each one?

- What was the combined highest value across all reportable accounts?

- Are there joint accounts that still need to be counted?

- Are closed accounts still relevant because they existed during the year?

- Does the foreign-account picture also raise a FATCA reporting issue?

That is the practical test.

The IRS says FBAR filing may be required if the aggregate value of foreign financial accounts exceeds $10,000 at any time during the year. The IRS also states that the due date is April 15, with an automatic extension to October 15.

That means “ready” is not a feeling. It is a documented position.

This is also why many people who think they are nearly done are not actually done.

Why does FBAR filing catch people late, even when the return seems simple?

Because the tax return and FBAR filing are not the same job.

A return can look straightforward:

- W-2 income

- a few 1099s

- standard deductions

- no obvious business income

Then the foreign side starts showing up:

- one NRE account

- one NRO account

- One old fixed deposit

- one joint family account

- one foreign brokerage balance

Individually, none of these may look large.

Together, they can create an FBAR filing requirement.

This is one of the most common blind spots for taxpayers with India-linked finances. They do not underestimate the law. They underestimate the way ordinary accounts add up.

The yearly filing pattern becomes easier to understand when it is seen as part of the same season as the return. FBAR Filing for Indians is useful here because it puts the tax-year filing and foreign-account timing in one frame.

Which accounts should be checked before deciding that FBAR filing is not required?

This is where many mistakes happen.

The accounts that get skipped most often are not unusual. They are ordinary accounts that do not feel urgent.

You should check:

- NRE accounts

- NRO accounts

- foreign savings accounts

- fixed deposits

- joint accounts

- brokerage accounts

- older accounts with low activity

- accounts closed during the year, but still active for part of it

The biggest mistake is not misunderstanding the rule. The biggest mistake is leaving accounts out before you even apply the rule.

A very common example looks like this:

- Account 1: $3,400

- Account 2: $2,600

- Account 3: $2,900

- Account 4: $1,500

None of these balances seems dramatic. Combined, they may cross the line for FBAR filing. The IRS says the threshold is based on the combined value of foreign financial accounts, not one account alone.

That is why the account list comes before the filing decision.

If older years are part of your concern, knowledge of Late FBAR Filing helps you take the right current-year steps.

How is FATCA reporting different from FBAR filing?

This is where even careful filers get tripped up.

FBAR filing and FATCA reporting are related, but they are not the same requirement.

The IRS says Form 8938 is used to report specified foreign financial assets if the applicable threshold is met. The IRS also states that Form 8938 and FBAR are separate requirements, and one does not replace the other.

That means:

- you may need FBAR filing

- you may need FATCA reporting

- you may need both

A person can report foreign interest income correctly and still miss the asset-disclosure side.

That is why FATCA reporting should never be treated like a side note once foreign assets are part of the filing picture.

Why do tax consultants separate “account balance” from “account ownership”?

Because those are two different risk points.

A filer may think:

- “It is only a joint account.”

- “The money belongs to my parents.”

- “My name is there only for convenience.”

That does not automatically remove the account from the filing analysis.

This is exactly why experienced tax consultants spend time building the account list properly before deciding what belongs in FBAR filing and what does not.

The hidden risk is rarely one dramatic mistake. It is usually one assumption that never got checked.

That may be:

- a joint holder assumption

- an old-account assumption

- an “inactive means irrelevant” assumption

- a “small means safe” assumption

Those are ordinary assumptions. They are also the ones that create last-minute problems.

Why should a tax expert check residency before FBAR filing is treated as final?

Because residency affects the whole filing structure.

A lot of people assume immigration status and tax status are the same. They are not.

A tax expert will check residency first because it can affect:

- What income belongs on the return

- whether worldwide reporting applies

- How FATCA reporting thresholds are evaluated

- whether treaty issues need attention

That is why a foreign-account filing should not be treated as a stand-alone issue. It has to fit the return correctly.

If that part has not been settled, the filing can look complete while the structure underneath is weak.

For that reason, knowing Resident vs Non-Resident becomes crucial.

And if the facts are mixed, Tax Consultations is the better move than filing off assumptions and hoping the structure holds.

What documents should be ready before April 15 if FBAR filing may apply?

If the foreign-account side is active, the paperwork should be assembled before the final filing push.

That usually includes:

U.S. records

- W-2s

- 1099s

- brokerage statements

- last year’s return

- payment records if estimates were made

Foreign-account records

- full-year bank statements

- fixed deposit statements

- brokerage summaries

- records for joint accounts

- records for accounts closed during the year

- foreign interest summaries, if available

Filing-position records

- visa and travel history if residency is unclear

- spouse details if filing jointly

- any prior IRS notices connected to past filing gaps

This is where professional tax services help most. The paperwork itself is not the issue. The issue is that collecting the right records before the deadline forces guesswork.

Why do professional tax services matter more close to April 15?

Because this is where the filing process becomes fragile.

Late in the season, people stop asking broad questions and start asking narrow ones:

- Can I leave this one account out for now?

- Can I just file and fix the rest later?

- Is an extension enough?

- Can this one detail wait?

That change in mindset is the real risk.

Strong professional tax services protect the order of work:

- Confirm the filing position

- gather the account list

- test FBAR filing

- test FATCA reporting

- Prepare the return

- separate filing timing from payment timing

That order is what keeps the final week from becoming a cleanup week.

This is also why the best tax filing service is not the one that files first. It is the one that sends one careful filing instead of one rushed filing, plus one correction later.

What payment issue is most often missed before April 15?

The simplest one.

People focus on filing and forget that filing and payment are not the same decision.

The IRS states that April 15 is generally the deadline to file and pay for most taxpayers. The IRS also states that an extension gives extra time to file, not more time to pay tax due.

That creates a common mistake:

- the filer gets an extension

- assumes the main pressure is gone

- does not handle the payment side

- later faces interest or penalties

This is one of the most overlooked pre-April 15 compliance problems because it does not look like a foreign-account problem. But it can still make a correct return more expensive.

If the deadline is already slipping or the filing window is nearly gone, know about Missed IRS Deadline.

What does an FBAR-ready filer do differently before April 15?

Not much, but they do it in the right order.

A filer who is truly ready has already:

- built a full foreign-account list

- checked the highest balances, not just year-end balances

- separated FBAR filing from FATCA reporting

- checked ownership, not just balances

- confirmed whether the return and the foreign side fit together

- checked the payment position before the deadline

That is what readiness looks like.

It is not speed.

It is not confidence without facts.

It is not “I think I included everything.”

It is a clean, supportable position.

This is where experienced tax consultants and a steady tax expert make the most difference. They do not make the deadline disappear. They make the filing stronger before the deadline arrives.

FAQs

What is the deadline for tax year 2025 returns?

For most individual calendar-year filers, the deadline is April 15, 2026. The IRS says this is generally the date to file and pay.

Is FBAR filing separate from FATCA reporting?

Yes. The IRS states that FBAR and Form 8938 are separate requirements, and one does not replace the other.

What is the most common FBAR mistake before April 15?

The most common mistake is leaving out one or more foreign accounts before calculating the total. The IRS rule is based on the combined value of foreign financial accounts.

Do joint accounts matter for FBAR filing?

They can. Account ownership is one of the most common weak points in late-stage filing. A joint account should not be ignored just because the funds feel like family money.

Does an extension solve the payment problem?

No. The IRS states that an extension gives more time to file, not more time to pay tax due.

What makes the best tax filing service close to April 15?

A process that checks the facts before filing. Near the deadline, speed without structure creates avoidable risk.

Final word

If the question is “Is your FBAR ready?” the answer should not be based on memory or comfort.

It should be based on:

- a full account list

- correct balances

- clear ownership

- proper separation of FBAR filing and FATCA reporting

- a filing plan that still holds under deadline pressure

That is what pre-April 15 compliance really means.

Let CrescentTaxFiling tax advisors confirm yours.

Visit the homepage to lock in your review before the deadline approaches.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional tax advice. Tax laws and reporting rules can change. You should discuss your facts with a qualified tax expert, tax consultants, or a provider of professional tax services before making filing decisions.