If there are 45 days left until April 15, you still have enough time to file on time.

That matters.

For many Indians in USA, tax filing is not just about one return. It often includes U.S. income, Indian bank accounts, old fixed deposits, family-linked accounts, and foreign reporting rules that do not leave room for guesswork.

The federal due date for most individual calendar-year filers for tax year 2025 is April 15, 2026.

That date is fixed. Your preparation time is not.

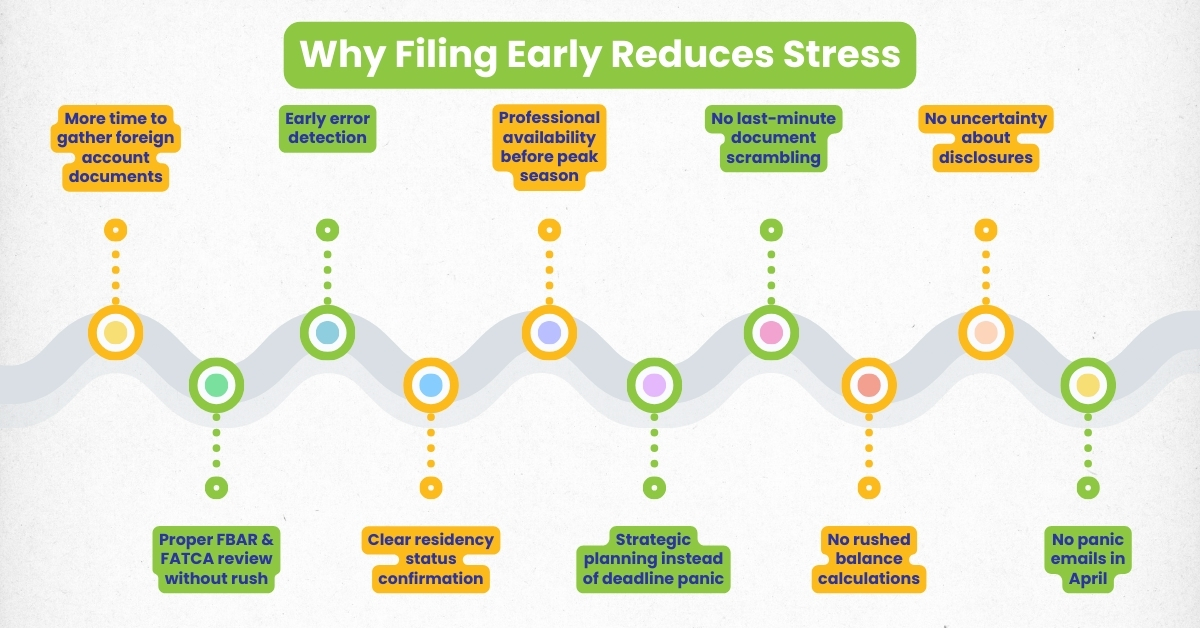

If you want this filing season to stay calm, the next 45 days should be used for review, not last-minute decisions.

A good place to start is Individual Tax Filing Services, especially if you want the filing process organized before the deadline starts driving every decision.

Why should Indians in USA start tax filing services before March ends?

Because waiting until March changes the quality of your work.

When you start early, you:

- Collect records properly

- Check foreign accounts carefully

- Fix missing items without panic

- Review FBAR filing and FATCA reporting before submission

When you start late, you:

- rush

- estimate

- skip reviews you meant to do

- Discover problems after the return is already built

This is the practical reason many people benefit from early tax filing services. It is not about filing faster. It is about filing with enough space to check what matters.

The season itself makes more sense when you are aware of the IRS Deadline 2026.

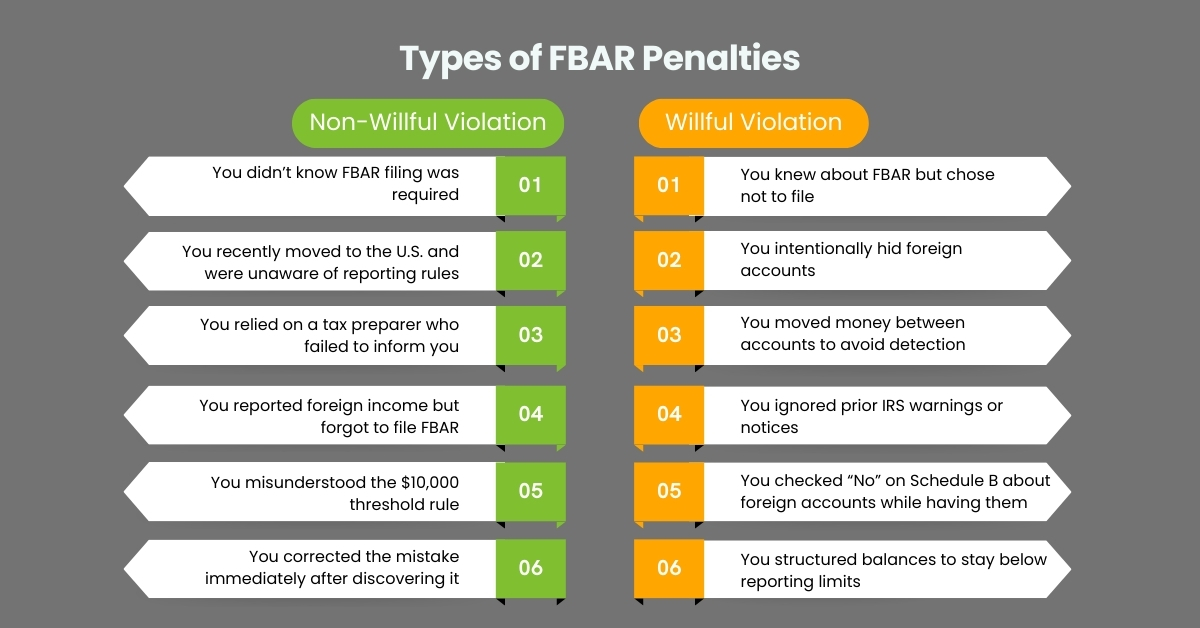

Why does FBAR filing need to be checked first for many Indians in USA?

Because foreign account reporting is usually the first surprise.

The IRS says you may need FBAR filing if the aggregate value of your foreign financial accounts exceeded $10,000 at any time during the year. The IRS also states that the FBAR due date is April 15, with an automatic extension to October 15.

Two words cause most of the confusion: aggregate value.

It is not one account over $10,000.

It is all the qualifying foreign accounts added together.

That may include:

- NRE accounts

- NRO accounts

- savings accounts

- fixed deposits

- some brokerage accounts

- certain joint accounts

A very common example looks like this:

- NRE account: $4,000

- NRO account: $2,800

- fixed deposit: $3,900

None looks large alone. Together, they can trigger FBAR filing.

This is where time matters. If you still have 45 days, you can check full-year statements and identify the highest balance properly. If you wait, you end up guessing.

If you are unsure how the current filing cycle works for foreign reporting, research about FBAR Filing for Indians in USA.

And a good point is to know the implications of Late FBAR Filing.

Why is FATCA reporting a separate checklist item from FBAR filing?

Because they are not the same rule.

The IRS states that Form 8938 is used to report specified foreign financial assets if you meet the filing threshold for your situation. The IRS also states clearly that Form 8938 and FBAR are separate requirements, and one does not replace the other.

That means some taxpayers may need:

- A tax return

- FBAR filing

- FATCA reporting

And they may need all three in the same season.

This catches many people off guard because they assume foreign income reporting and foreign asset reporting are the same thing. They are not.

A return can be correct on income and still incomplete on disclosure.

If you want the broader filing basics before you get into the reporting layers, know everything about US Tax Filing for NRIs in the USA.

Why should a tax expert review residency before anything else?

Because residency affects the rest of the return.

Many Indians in USA confuse immigration status with tax status. That creates problems.

Your tax residency can affect:

- whether worldwide income is reportable

- whether FATCA reporting thresholds apply

- whether treaty rules may matter

- what type of return you should file

If the residency assumption is wrong, everything after it may need to be redone.

That is why this should be checked early, not when the return is almost finished.

The first thing to know is Resident vs Non-Resident Alien, as the differentiation helps determine residency.

If the situation is not clear, Tax Consultations is the right step before you make filing decisions based on guesswork.

Why do professional tax services help reduce last-minute mistakes?

Because most filing mistakes begin as process mistakes.

They usually look like this:

- starting the return before gathering all records

- checking income but not foreign accounts

- forgetting a joint account

- assuming a small balance does not matter

- treating an inactive account as if it does not exist

- thinking an extension fixes everything

Good professional tax services slow the process down in the right places.

That is what keeps small errors from turning into larger ones after filing.

The practical sequence should look like this:

1. Collect all records

You need:

- W-2s

- 1099s

- brokerage statements

- India bank statements

- FD details

- interest certificates

- records of major transfers

- prior-year return

2. Confirm residency

Before the return is built.

3. Review foreign accounts

Before software decisions are made.

4. Check FBAR filing

Using actual balances, not memory.

5. Check FATCA reporting

Separately from FBAR.

6. Build the return

Only after the facts are clean.

This is why early professional tax services are useful. They do not just prepare forms. They protect the order of work.

Why do tax consultants say 45 days is the best time to build a full checklist?

Because 45 days gives you time to divide the work.

That is long enough to review properly.

It is short enough that the deadline still matters.

Here is the cleanest way to use the next 45 days.

Days 45 to 35

- gather all U.S. and India records

- confirm whether any accounts were opened, closed, or changed

- review residency

- list every foreign account you can think of

Days 34 to 25

- determine whether FBAR filing applies

- check whether FATCA reporting may apply

- identify missing statements

- review large transfers or unusual balances

Days 24 to 15

- prepare the draft return

- reconcile income

- estimate payment due

- decide whether an extension is needed

Days 14 to 7

- review final figures

- confirm foreign disclosures

- double-check names, account details, and ownership

Final week

- file

- save all confirmations

- store copies of statements and returns together

This is simple. That is why it works.

The goal is not to make tax season complicated. The goal is to prevent avoidable pressure.

Why is the best tax filing service not the fastest one?

Because speed without review creates cleanup.

A return can be filed quickly and still have:

- missing foreign disclosures

- incorrect assumptions about ownership

- overlooked asset reporting

- a weak extension plan

- avoidable follow-up work

That is why the best tax filing service is usually the one that forces review before submission.

For many Indians in USA, that means checking:

- foreign balances

- FBAR filing

- FATCA reporting

- residency

- payment timing

before the return is sent.

If you need broader planning beyond this filing, Tax Planner Services can be relevant after the immediate return is complete. But the current priority is this season, not next season.

Why should Indians in USA understand what an extension really does?

Because extensions are often misunderstood.

An extension gives more time to file. It does not give more time to pay if tax is due. That is standard IRS guidance for extensions.

So if you are not ready, filing an extension may still be smart. But it should be part of a plan.

It should not be treated as:

- a full delay of all obligations

- a replacement for reviewing foreign accounts

- a way to avoid calculating tax due

This is exactly why waiting until the last week is risky. By then, people often ask about extensions because they ran out of time, not because they made a filing decision early.

FAQs

What is the deadline for tax year 2025 returns?

For most calendar-year individual filers, the due date is April 15, 2026.

Do Indians in USA need FBAR filing for NRE and NRO accounts?

They may. If the total value of foreign financial accounts exceeds $10,000 at any point during the year, FBAR filing may be required.

Is FATCA reporting the same as FBAR filing?

No. The IRS states that they are separate filing requirements. One does not replace the other.

Should I start my tax filing services before March?

Yes. Starting before March gives you time to review records, check foreign reporting rules, and reduce errors before the deadline gets close.

Why do tax consultants focus on residency first?

Because residency can affect what income and foreign assets must be reviewed. If that starting point is wrong, the rest of the return may need to change.

Is an extension enough if I still have not reviewed my foreign accounts?

No. An extension may give more time to file, but it does not remove the need to review FBAR filing, FATCA reporting, or payment obligations properly.

Final word

If there are 45 days left before April 15, you are still in a good position.

But only if you use that time for review.

For Indians in USA, the biggest filing problems usually begin when:

- Foreign accounts are checked too late

- FBAR filing is discovered too late

- FATCA reporting is reviewed too late

- Residency is guessed too late

That is what this checklist is meant to prevent.

Use the next 45 days well.

Collect records early.

Review foreign accounts calmly.

Check the filing rules before you build the return.

That is how April stays manageable.

If you would like to review your FBAR or FATCA position calmly this February, a brief conversation with a tax expert can help you move forward with confidence.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional tax advice. Tax laws and reporting rules are complex and can change. You should review your specific situation with a qualified tax expert or professional tax services provider before making tax decisions.