The last few days before a tax deadline are when small mistakes turn into larger problems.

That is true in any filing season. It becomes more serious when foreign accounts, foreign assets, old balances, and cross-border reporting are part of the return.

For tax year 2025, the filing date for most calendar-year individual returns is April 15, 2026. The IRS states that clearly on its filing page. If you wait until the last minute, the biggest danger is not only filing late. The bigger danger is filing before you have checked what should have been checked.

For many Indians in USA, that means the pressure is not just about one form. It is about:

- a tax return

- FBAR filing

- possible FATCA reporting

- payment timing

- account ownership

- residency position

This is where last-minute filing becomes risky.

If your filing still feels disorganized, Individual Tax Filing is the cleanest place to start building order before the deadline takes over.

Why is last-minute filing risky for tax filing services?

Because the return stops being a review and becomes a race.

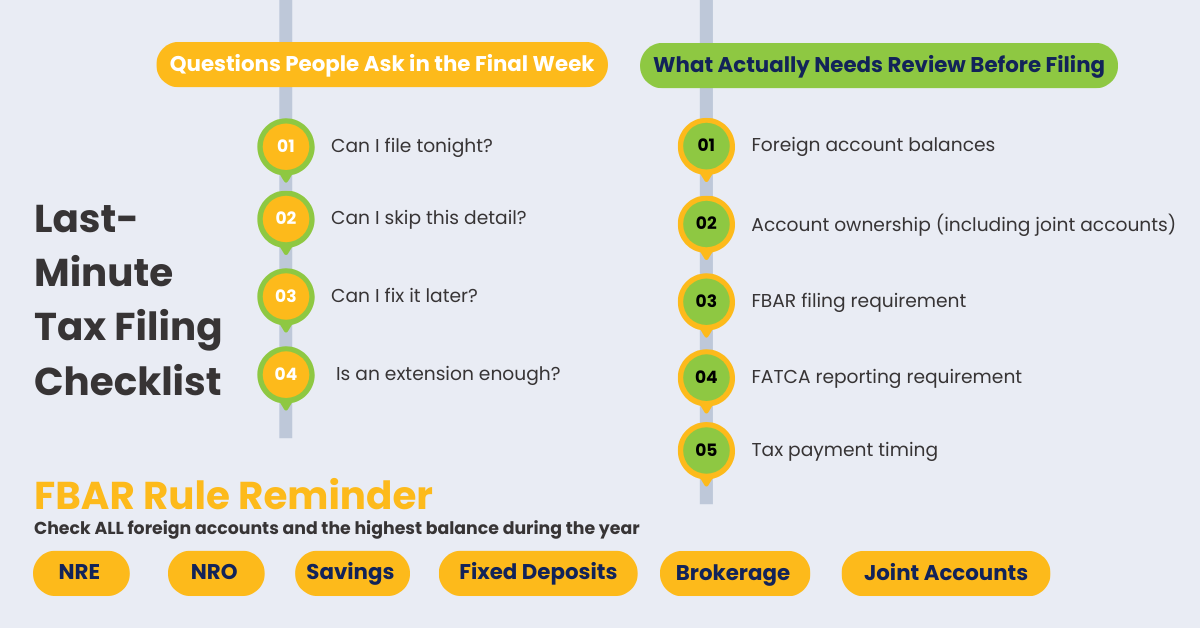

In the last week before April 15, most people stop asking careful questions. They start asking urgent ones:

- Can I file tonight?

- Can I skip this one detail?

- Can I fix this later?

- Is an extension enough?

That change in thinking is the problem.

When filing becomes a rush, the work that gets cut is usually the work that mattered most:

- checking foreign balances

- verifying account ownership

- confirming whether FBAR filing applies

- checking whether FATCA reporting applies

- reviewing payment timing

That is why late filing pressure creates weak decisions. It is not because the forms are impossible. It is because the review gets cut short.

This is why strong tax filing services focus on sequence before submission.

If the season still needs a clear structure, IRS Deadline 2026 puts the filing timeline in order.

Why does FBAR filing become one of the biggest last-minute mistakes to avoid?

Because it is usually discovered too late.

The IRS says FBAR filing may be required when the combined value of foreign financial accounts exceeds $10,000 at any point during the year. The IRS also states that the FBAR due date is April 15, with an automatic extension to October 15. The rule sounds simple. The mistake is that people apply it too narrowly.

They often think:

- one account

- one balance

- one year-end number

The real review is broader:

- all foreign accounts together

- The highest value during the year

- all qualifying accounts, including ones not used often

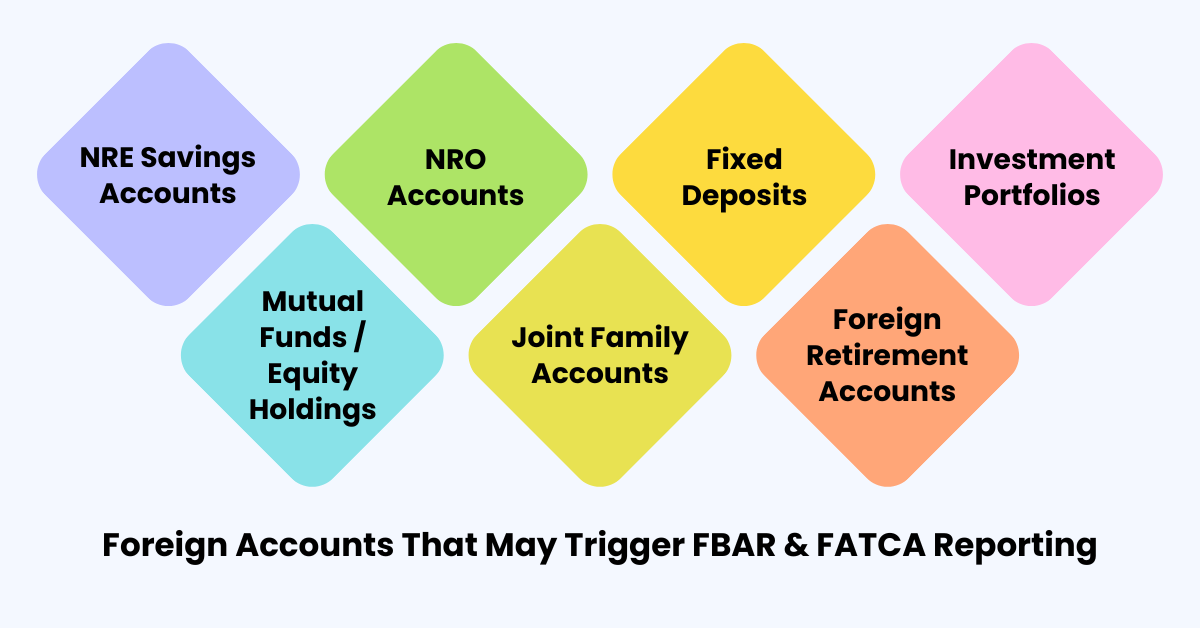

That may include:

- NRE accounts

- NRO accounts

- savings accounts

- fixed deposits

- brokerage accounts

- joint accounts

This is where the last-minute error happens. A filer checks one account and forgets the others. Or they use a year-end balance instead of the highest balance during the year.

That is not a minor detail. It can change whether FBAR filing is required at all.

This is exactly why FBAR Filing for Indians in USA matters before the final filing push. It places the foreign reporting cycle in the same frame as the return itself.

If prior years are part of the concern, Late FBAR Filing becomes part of the last-minute review as well.

And if the return clearly includes foreign accounts, FBAR Filing FATCA is the right service page to use before filing for guesswork.

Why is missing FATCA reporting a common last-minute filing mistake?

Because a return can look complete when it is not.

The IRS says Form 8938 is used to report specified foreign financial assets when the applicable threshold is met. The IRS also says that Form 8938 and FBAR are separate requirements. One does not replace the other.

That creates a common filing mistake.

A taxpayer reports:

- wages

- interest

- dividends

- foreign income

and assumes the foreign side is fully handled.

It may not be.

FATCA reporting is not the same as reporting foreign income. It is a separate asset-review question. That means the return can be accurate on income and still incomplete on disclosure.

This is especially risky in the last few days because FATCA reporting decisions are not good “quick decisions.” They depend on:

- the type of foreign assets involved

- thresholds that depend on filing facts

- what else has already been disclosed

That is why FATCA reporting is one of the most common last-minute filing mistakes to avoid.

If the larger filing structure still needs to be made clear before the final push, US Tax Filing helps ground the process before the disclosure details are layered in.

Why should a tax expert check residency before the return is submitted?

Because once the return is almost ready, people do not want to reopen the foundation.

That is exactly why this gets missed.

Residency can change:

- What income is reportable

- whether some foreign assets need closer review

- How FATCA reporting is evaluated

- Which return is even appropriate

This is not a small technical point. It can change the structure of the filing itself.

A common last-minute mistake is assuming:

- A visa status answers the tax question

- A prior-year filing position automatically still works

- A short travel difference is not important

Those assumptions can be wrong.

That is why Resident vs Non-Resident belongs in the review before the return is treated as final.

If the facts are mixed, Tax Consultations is the better option than forcing a rushed conclusion.

Why do professional tax services help prevent last-minute errors?

Because the last-minute problem is usually a process problem.

The return is not always difficult. The process is just out of order.

Common last-minute patterns look like this:

- enter W-2 income

- Enter 1099 income

- think the return is mostly done

- Remember the foreign account later

- Try to squeeze that review into the final day

That is exactly backwards.

The stronger process is:

- gather all records

- confirm residency

- List foreign accounts and assets

- test FBAR filing

- test FATCA reporting

- build the return

- Confirm payment or extension timing

That is where professional tax services help most. They do not make the rules easier. They keep the work in the right order.

Why is waiting until April 15 risky even if the return is ready?

Because the return is not the only deadline issue.

The IRS states that April 15 is generally the deadline to file and pay. The IRS also states that taxpayers who need more time to file should request an extension, but an extension gives more time to file, not more time to pay tax due.

That creates one of the most common last-minute mistakes:

- a taxpayer files or plans an extension

- assumes the deadline pressure is handled

- does not pay what should be paid

- Later faces interest and penalties

That is not a filing mistake alone. It is a timing mistake.

This is why the final review should always ask two separate questions:

- Can the return be filed on time?

- If tax is due, can it be paid on time?

Treating those as one question is a last-minute error that many people do not catch until later.

If the deadline has already become a problem, know what it means to be on the missed IRS Deadline

Why are old accounts and “small” accounts dangerous in the final week?

Because they are easy to dismiss.

A filer in the last week often says:

- It is a small account.

- It is inactive.

- It is old.

- It is mostly family money.

- It probably does not matter.

That is where many late errors come from.

The account types that get ignored most often are:

- an old NRO account with a modest balance

- a fixed deposit that has not been touched in a long time

- a joint account held for convenience

- a dormant brokerage account with no recent trades

These are dangerous because they do not feel active enough to matter.

But FBAR filing is not about whether an account feels important. It is about whether it is reportable.

That is why “small” does not mean “safe.”

Why do tax consultants warn against filing first and fixing later?

Because that approach usually creates more work than it saves.

Last-minute filers often tell themselves:

- I will file now and amend later.

- I will deal with the foreign side next week.

- I will sort the account issue after the deadline.

That is weak filing logic.

Corrections take:

- extra time

- extra review

- extra explanation

- sometimes more stress than the original filing

That is why seasoned tax consultants try to prevent corrections instead of planning for them.

It is better to file one careful return than one rushed return plus one cleanup round.

Why is the best tax filing service built on review, not speed?

Because speed only helps after the facts are correct.

That is the point most people miss late in the season.

The best tax filing service should force these checks before submission:

- foreign account totals

- account ownership

- asset disclosure review

- FBAR filing

- FATCA reporting

- payment timing

- extension decisions if needed

When those checks are cut short, the return may still go out on time. But the filing is weaker than it looks.

That is why last-minute filing is risky. The deadline pushes people toward speed at exactly the point where they need patience.

FAQs

What is the filing date for tax year 2025?

For most individual calendar-year filers, the IRS deadline is April 15, 2026. The IRS also states this is generally the deadline to file and pay.

Is FBAR filing the same as FATCA reporting?

No. The IRS states they are separate requirements, and one does not replace the other.

What is the biggest last-minute filing mistake?

The biggest mistake is filing before foreign accounts, asset disclosures, payment timing, and residency have been fully reviewed.

Can an extension fix a last-minute filing problem?

It can help with filing time, but the IRS states that an extension does not extend the time to pay tax due.

Why should a tax expert review the return before filing?

Because late-season mistakes are usually not about math. They are about what was never reviewed.

What makes the best tax filing service near the deadline?

A process that checks facts before submission. Near the deadline, speed without review is risky.

Final word

The last few days before April 15 are when avoidable mistakes become easy to make.

That is why the safest move is not to rush harder.

It is to slow down the right parts:

- Check foreign accounts

- Test FBAR filing

- Test FATCA reporting

- Confirm residency

- Separate filing timing from payment timing

Those are the last-minute tax filing mistakes to avoid.

If you would like to review your FBAR or FATCA position calmly this February, a brief conversation with a tax expert can help you move forward with confidence.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional tax advice. Tax rules and reporting rules can change. You should review your specific facts with a qualified tax expert, tax consultants, or a provider of professional tax services before making filing decisions.